Back in 2011, a writer at Techi.com made an argument that most of the entertainment industry dismissed as fringe thinking: pirates weren’t the enemy. They were a symptom. The real problem was an industry charging $25 for a DVD that cost pennies to replicate, refusing to sell movies digitally at reasonable prices, and treating every customer like a criminal while actual criminals downloaded whatever they wanted for free. The argument was simple: piracy wasn’t about greed. It was about value. And if Hollywood couldn’t figure that out, Netflix would do it for them.

Fifteen years later, that thesis looks like prophecy. Netflix is now a $300 billion company. Blockbuster is a museum piece. The DVD section at Best Buy has shrunk to a single dusty shelf near the back, wedged between car accessories and printer ink. And piracy? It went away for a while, then came roaring back the moment streaming got expensive and complicated again.

This is the story of how a bunch of torrent sites accidentally designed the modern entertainment industry.

The 2011 Thesis: Pirates as Market Correctors

The conventional wisdom in 2011 was that piracy was theft, full stop. The MPAA ran ads comparing downloading a movie to stealing a car. Studios lobbied Congress for increasingly aggressive takedown laws. Every pirated copy was counted as a lost sale, a framing so mathematically absurd that even the researchers the industry hired struggled to defend it.

But the data told a more complicated story. In 2006, the DVD market peaked at roughly $16.3 billion in the United States alone. And yet the most-pirated films of that era were also among the highest-grossing at the box office. People weren’t pirating instead of watching. They were pirating because the industry had structured legitimate access to be as inconvenient and expensive as possible.

Want to watch a movie that came out three years ago? You could buy the DVD for $19.99, rent it from a Blockbuster that charged late fees and required you to drive somewhere, or wait for it to show up on cable at a time you may or may not be home. Alternatively, you could download it in 45 minutes and watch it whenever you wanted on any device you owned.

The choice wasn’t really about money. It was about friction. And pirates had figured out how to eliminate friction entirely.

Economists who studied this period found weak or negative correlation between piracy rates and sales declines. The real story was that piracy was functioning as a price signal. Consumers were communicating, loudly and illegally, that they were willing to pay for content but not at the prices and with the restrictions being imposed on them. DRM that prevented you from playing a disc you legally purchased on your laptop. Regional encoding that meant a DVD bought in Europe wouldn’t play in the US. Windows Media files that expired after 30 days even though you’d paid for them.

The 2011 thesis put it plainly: the home movie industry needed pirates to survive, because pirates were the only honest market feedback the industry was getting. Everyone else had just stopped buying.

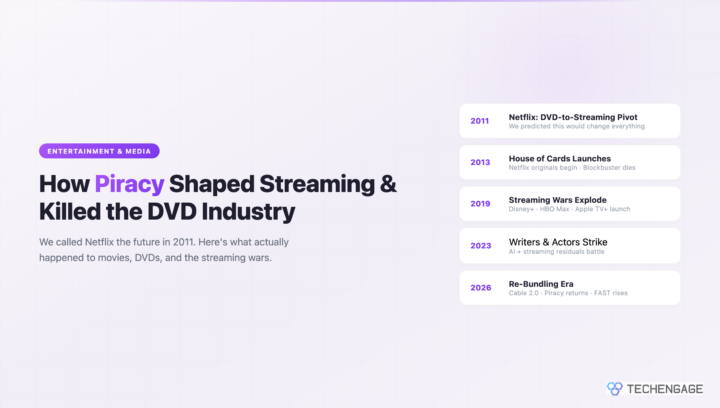

Netflix’s DVD-to-Streaming Pivot

Netflix in 2011 was a $3 billion company that mailed red envelopes. Reed Hastings had launched streaming as a complement to the DVD service in 2007, and by 2011 about 23 million subscribers were using it. Then Hastings made one of the most consequential blunders in corporate history and accidentally accelerated the future of entertainment.

In July 2011, Netflix announced it would split its DVD and streaming services, raising the combined price by 60 percent. The outcry was immediate and overwhelming. The company lost 800,000 subscribers in a single quarter. Its stock dropped 77 percent from peak to trough over the following months. Hastings issued a public apology that somehow made things worse by announcing the DVD service would be rebranded as “Qwikster,” a name so widely mocked it was abandoned within three weeks.

But here’s what the coverage mostly missed at the time: Hastings wasn’t wrong about the direction. He was just wrong about the speed and the execution.

The Qwikster disaster forced Netflix to focus almost entirely on streaming. They couldn’t afford to be mediocre at two things simultaneously, and the subscriber revolt made clear that the future customers wanted was digital. By 2012, Netflix had recovered its subscriber count. By 2013, it had more streaming subscribers than any cable network in America. Hastings later described the Qwikster incident as a necessary humbling, a moment that clarified exactly what Netflix was and what it needed to become.

What Hastings had seen, and what the 2011 article had also identified, was that the studios’ licensing agreements were a ticking clock. Netflix was paying relatively modest fees for vast streaming libraries because the studios didn’t yet believe streaming was real competition. Once they figured it out, they’d pull their content and demand much more money. The only sustainable path was building original content that Netflix owned outright. Content that couldn’t be yanked back by a studio that suddenly decided to launch its own service.

The strategic logic was sound. The execution would prove it.

The Death of Physical Media

Blockbuster filed for bankruptcy in September 2010 with $1 billion in debt. At its peak, the company had 9,000 stores worldwide and 60,000 employees. The last corporate-owned Blockbuster store in the United States closed in January 2014. One franchise location in Bend, Oregon became a cultural attraction and the subject of a documentary. People visit it like a monument.

The DVD numbers tell the full story. From that $16.3 billion peak in 2006, US physical media revenue fell to $7.8 billion in 2011, the year the original article was written. By 2015 it had dropped to $3.9 billion. By 2020 it was around $2.1 billion. By 2023, industry analysts placed it at roughly $1.3 billion, almost entirely driven by collector editions, 4K UHD releases for videophiles, and catalog titles that older consumers still prefer to own physically.

Blu-ray actually had a brief renaissance in the early 2010s as HD televisions became standard, and the format still sells in the collector market. But it never replaced DVD’s mass-market role, partly because streaming offered good-enough quality to most viewers, and partly because the format war with HD-DVD (which Blu-ray won in 2008) had exhausted consumer goodwill toward physical media upgrades.

Best Buy, which once dedicated entire aisles to DVDs and CDs, began quietly contracting its physical media section around 2018. By 2023, the company announced it would phase out physical media sales entirely, following Target’s decision to significantly cut back its disc inventory. Walmart, the largest physical media retailer in the US, maintains a nominal section but has reduced floor space consistently for a decade.

The collectors-only niche is real and surprisingly passionate. The Criterion Collection, which releases restored and curated editions of art-house and classic films, actually grew its business through this period by leaning into the premium physical product. Their releases routinely sell out. But that’s a hobbyist market, not a mass market. Physical media is now where vinyl was in 1995: not dead, but irrelevant to most people’s daily lives.

House of Cards and the Original Content Revolution

February 1, 2013. Netflix releases all 13 episodes of House of Cards simultaneously. The entire season, at once, available to stream. No weekly schedule, no network notes, no commercial breaks, no pilot-and-pickup process. Just 13 hours of prestige political drama starring Kevin Spacey and Robin Wright, directed in part by David Fincher, delivered all at once to anyone with a $7.99 monthly subscription.

The entertainment industry treated this like a stunt. It became a template.

Netflix had paid $100 million for two seasons upfront without seeing a pilot, a decision that stunned traditional networks, which had elaborate development processes designed to minimize exactly this kind of financial risk. The conventional wisdom was that Netflix had overpaid and overreached. The unconventional reality was that Netflix had data that nobody else had. They knew, with remarkable precision, how many of their subscribers had watched the British original House of Cards. They knew how many had watched David Fincher films. They knew how many had watched Kevin Spacey. The Venn diagram was large enough to justify the bet.

House of Cards won three Primetime Emmy Awards in its first year, becoming the first streaming series nominated for the top Emmy award. The cultural signal was unmistakable: streaming wasn’t lesser television. It was television, full stop, and in some respects it was better, free from advertiser restrictions, network standards, and the tyranny of the 22-episode season order.

Orange Is the New Black followed later in 2013. Daredevil, Narcos, Stranger Things, The Crown: each successive hit validated the model and raised the stakes. Amazon, which had been experimenting with its Prime Video service since 2011, scored its own prestige wins with Transparent and The Man in the High Castle. By 2015, the question wasn’t whether streaming could produce quality content. The question was whether traditional television could compete.

The studios and networks watched all of this and drew the obvious conclusion. If Netflix could do it, they could do it themselves. And they had something Netflix desperately needed: decades of beloved intellectual property.

The Streaming Wars (2019-2022)

Disney+ launched November 12, 2019. In its first day, the service crashed repeatedly under demand. Within a week it had 10 million subscribers. By March 2020, when a global pandemic locked most of the developed world indoors, it had 50 million. The Disney intellectual property arsenal, including Marvel, Star Wars, Pixar, National Geographic, and the Disney vault itself, proved to be exactly as powerful a streaming weapon as anyone had suspected.

HBO Max launched in May 2020. Peacock (NBCUniversal) in July 2020. Paramount+ in March 2021, rebranded from the earlier CBS All Access. Apple TV+ had actually arrived first, in November 2019, bundled with device purchases and priced at $4.99 a month, a price point that signaled Apple was buying cultural credibility, not immediate profit.

The financial logic for each of these launches was identical and, in retrospect, slightly delusional. Every major media company looked at Netflix’s valuation, which by 2020 had exceeded $200 billion, and concluded that streaming subscribers were worth dramatically more than traditional cable subscribers or box office dollars. Wall Street was rewarding subscriber growth above all else, which meant every studio needed subscriber numbers, which meant every studio needed a streaming service.

The content fragmentation that resulted was genuinely remarkable. Friends left Netflix for HBO Max. The Office left for Peacock. Disney pulled its library from Netflix. Marvel and Star Wars content became Disney+ exclusives. By 2021, a household that wanted to watch the full range of prestige content that had previously been available on two or three services now needed at least six or seven subscriptions, spending anywhere from $60 to $100 per month on streaming alone.

This was, as the entertainment press noted with increasing frequency, starting to look a lot like cable.

Subscription Fatigue and the Great Re-Bundling

The breaking point arrived somewhere around 2022-2023. Netflix raised its standard plan price from $9.99 to $15.49. HBO Max and Disney+ both raised prices. Hulu raised prices. Apple TV+ raised prices. Peacock raised prices. The average American household with four or more streaming subscriptions was now spending as much monthly as they’d paid for cable a decade earlier, except with more decision fatigue and fewer live sports.

Subscriber growth began stalling across the industry. Netflix reported its first subscriber loss in a decade in Q1 2022, down 200,000 accounts, and its stock fell 35 percent in a single day. The Wall Street growth story that had justified the entire streaming buildout suddenly looked precarious.

The industry’s response was to do what industries always do when the original plan stops working: bundle things together and call it innovation. Disney announced a bundle combining Disney+, Hulu, and ESPN+ at a discount. Warner Bros. Discovery merged HBO Max and Discovery+ into Max. Comcast bundled Peacock with other services. Apple bundled Apple TV+ into Apple One with Music, Arcade, and iCloud storage.

By 2024, the structure of the streaming market had converged toward three or four major bundled packages competing for household spending, which is, functionally, exactly what cable television was in 2005. Consumers had paid to dismantle cable, rebuilt it piece by piece over fifteen years, and were now paying roughly the same amount for a structurally similar product. The main differences are on-demand availability and the absence of regional sports blackouts, which is genuine progress, but barely qualifies as a revolution.

Reed Hastings had not, it turned out, defeated cable. He had evolved it.

Piracy’s Comeback

Piracy declined sharply between roughly 2012 and 2018. The reason was straightforward: Netflix, Spotify, and their equivalents had solved the friction problem. For $10 a month, a consumer could access more music and more film than any human could consume in a lifetime. Piracy wasn’t worth the effort or the risk when the legal alternative was better in almost every measurable way.

Then the streaming wars fragmented the libraries, raised the prices, and recreated the conditions that had made piracy attractive in the first place.

By 2023, analytics firms tracking piracy traffic were reporting significant increases. Muso, a piracy measurement company, found that film and TV piracy had risen notably compared to pre-pandemic levels. The correlation with streaming fragmentation was too obvious to ignore. When a show moved from Netflix to a competing service that cost $15 a month extra, some segment of viewers simply stopped paying.

Netflix’s password-sharing crackdown, which rolled out across most markets in 2023, accelerated the trend. For years, Netflix had tolerated account sharing as a user acquisition strategy, allowing an estimated 100 million households to access the service without paying. When the company began requiring paid add-on slots for shared accounts, some users converted to paying subscribers. Others simply left. A meaningful percentage returned to torrents.

The 2011 thesis had predicted exactly this dynamic: the industry’s willingness to tolerate piracy was directly correlated with the quality of its legal alternatives. Build something better and cheaper, piracy shrinks. Make the legal option expensive and inconvenient again, and piracy grows back. The entertainment industry had confirmed this theory twice, once by nearly eliminating piracy between 2012 and 2018, and again by reviving it between 2019 and 2024.

The Writers’ and Actors’ Strike of 2023

On May 2, 2023, the Writers Guild of America went on strike. On July 14, SAG-AFTRA joined them. For the first time since 1960, both writers and actors were on strike simultaneously. The combined work stoppage lasted 148 days for writers and 118 days for actors, making it the longest Hollywood strike in the modern era.

The core issues were streaming residuals and artificial intelligence. The residual system, which provides payments to writers and actors each time their work airs or streams, had been designed for broadcast television, where reruns and syndication generated substantial secondary income. Streaming had effectively eliminated residuals by replacing reruns with always-available libraries. A writer who had created a successful streaming series might receive a fraction of what they’d earned on a network show with comparable viewership, because the streaming numbers were largely hidden and the residual formulas hadn’t been updated to reflect how streaming actually worked.

The AI concerns were existential in a way the residual fight was not. Studios had begun exploring AI tools to generate scripts, create background actors digitally, and recreate deceased performers. The guilds wanted explicit contractual protections before those technologies became standard practice. Without them, the fear was that a decade of streaming-driven growth in content demand would be followed by an AI-driven collapse in demand for human creative labor.

The strikes ended with significant concessions. Streaming residuals were restructured, with new formulas based on viewership thresholds that actually tracked how people consumed content. AI protections were written into the contracts. Writers couldn’t be replaced by AI, and studios couldn’t use AI-generated material as a basis for lowballing fees. Actors won consent requirements for digital likeness use. The gains were real, though enforcement will take years to test fully.

What the 2023 strike demonstrated, more than anything, was that streaming had fundamentally altered the economics of Hollywood production without the people who make Hollywood content sharing in that transformation. Netflix’s model had been built partly on the assumption that it could pay less per project because it could aggregate more projects. The strikes were the inevitable correction.

FAST Channels and the Ad-Supported Revolution

Here is the entertainment industry’s most delicious irony: after spending fifteen years and hundreds of billions of dollars building subscription streaming to replace ad-supported television, consumers are now flocking to free, ad-supported streaming television. FAST (Free Ad-Supported Streaming TV) has become one of the fastest-growing segments in entertainment.

Tubi, owned by Fox Corporation, reported 80 million monthly active users in 2024. Pluto TV, owned by Paramount, has over 75 million. Amazon Freevee (now integrated into Prime Video’s free tier) and Peacock’s free tier add tens of millions more. These services offer thousands of channels and movies at no subscription cost, funded entirely by advertising, exactly like broadcast television, except delivered over the internet.

The content is largely catalog programming: older films, legacy television series, reality shows that have aged out of premium streaming. But the volume is enormous and the price is unbeatable. For a consumer who’s watching a 2004 procedural drama on a Tuesday night, there’s genuinely no reason to pay $18 a month for that content when Tubi has it free.

FAST channels are winning the subscription fatigue battle by simply opting out of the subscription model entirely. Their growth is partly a direct response to rising streaming prices. As Netflix and Disney+ raise rates, consumers allocate more time to free alternatives. The advertising market has followed them, with major brands shifting TV ad spending toward FAST platforms at a pace that surprised even the platforms themselves.

Netflix and Disney+ have both launched ad-supported tiers at lower price points, essentially admitting that the pure subscription model had reached its ceiling. The all-subscription future lasted about twelve years before the industry remembered that most people will accept ads if it means paying less money.

Where Entertainment Goes From Here (2026)

The entertainment industry in 2026 looks almost nothing like the entertainment industry of 2011, and almost nothing like what anyone predicted in 2019. The streaming wars that were supposed to produce one or two dominant winners have instead produced a complicated ecosystem of subscription tiers, bundled packages, free ad-supported services, and a piracy underground that never fully disappeared.

AI-generated content is now a real factor, not a theoretical one. Production studios are using AI tools for visual effects work, background generation, and localization at scales that have eliminated tens of thousands of entry-level production jobs since 2023. The AI writing tools that the WGA fought against in their 2023 contract are being used in preproduction development at studios that have found creative ways to work within the contractual language. The legal battles over what constitutes “AI-generated” material are ongoing in several jurisdictions.

Short-form content has become the most watched video format on earth, and neither Netflix nor Disney owns any of it. TikTok and YouTube together account for more daily video consumption hours than all subscription streaming services combined, according to multiple 2025 viewership analyses. The attention economy has shifted in ways that traditional entertainment economics can’t fully accommodate. A 90-minute film competes for attention against an infinite scroll of 30-second clips, and in terms of raw engagement hours, the clips are winning.

Sports rights have become the decisive battleground. Live sports are the one category of content that cannot be time-shifted, cannot be pirated effectively, and generates the kind of real-time communal viewing that streaming has otherwise eliminated. Amazon has NFL Thursday Night Football. Apple TV+ has Major League Baseball. Netflix has entered live sports with boxing events and WWE Raw. The scramble for live sports rights is replicating the content wars of 2019-2022, except with even higher financial stakes and longer contract windows.

The 2011 article’s central prediction, that Netflix would win and physical media would lose, turned out to be only half right. Netflix won, but it didn’t win cleanly or permanently. The industry it disrupted has reorganized around its model, raised prices until consumers pushed back, triggered a labor revolt, accidentally revived piracy, and is now chasing the next disruption before the current one fully plays out.

Pirates as market correctors remains accurate as a concept, even if the mechanism has changed. Today’s “piracy” is partly literal (torrents and streaming rippers) and partly behavioral. People sharing passwords. People rotating subscriptions monthly, subscribing to watch one show then canceling. People watching YouTube instead of paying for Netflix. The underlying behavior that the industry called theft in 2011 was always just consumers finding the path of least resistance to content they wanted. That path has shifted, but the principle hasn’t.

What the entertainment industry still hasn’t solved, fifteen years after that original article, is how to make legitimate access so simple and affordable that the path of least resistance runs straight through a legal service. Every time it gets close, pricing pressure or content fragmentation or executive overreach pushes the friction back up. And when friction goes up, alternatives multiply.

The industry that killed the DVD didn’t replace it with something simpler. It replaced it with something more complicated, more expensive, and more fragmented than cable ever was. That’s not what the pirates were asking for. It’s also not what Netflix promised in 2011. The gap between that promise and current reality is where the next disruption is already forming.

How did piracy influence the creation of streaming services?

Piracy exposed a fundamental market failure: consumers wanted convenient, affordable access to digital content and the entertainment industry wasn’t providing it. Services like Netflix recognized that if they could deliver content legally with less friction than piracy, at a reasonable price, people would pay. The dramatic decline in piracy between 2012 and 2018, coinciding with Netflix’s growth, validated the theory. Studios and networks initially licensed their libraries to Netflix cheaply because they underestimated streaming’s potential, which gave Netflix time to establish the model before the licensing deals expired.

When did DVD sales start declining?

US DVD sales peaked at approximately $16.3 billion in 2006 and began declining almost immediately afterward. The drop accelerated after Netflix launched its streaming service in 2007 and became significant by 2010-2011. By 2015, revenue had fallen below $4 billion. Physical media sales have continued declining every year since, with the market now primarily sustained by collector editions, 4K UHD releases for enthusiasts, and catalog titles. Best Buy announced it would phase out physical media sales entirely in 2023.

Why are there so many streaming services now?

When Netflix demonstrated that streaming subscribers could command dramatically higher valuations than traditional cable or broadcast viewers, every major media company concluded it needed its own service. Disney, NBCUniversal, WarnerMedia, Paramount, and Apple all launched services between 2019 and 2021. Each studio pulled its content from Netflix to use as exclusive bait for its own platform, fragmenting libraries that had previously been available in one place. The result was content scattered across six or more services, each charging separately, effectively recreating the cable bundle that streaming was supposed to replace.

What are FAST channels?

FAST stands for Free Ad-Supported Streaming TV. These are streaming services that require no subscription fee and are funded entirely through advertising, similar to broadcast television. Major FAST platforms include Tubi (owned by Fox), Pluto TV (owned by Paramount), and the free tiers of Peacock and Amazon’s streaming service. They primarily offer catalog content like older films and TV series but have grown rapidly as subscription streaming prices have risen. Tubi and Pluto TV each report over 75 million monthly active users, making them significant players in the streaming landscape despite their low profile compared to Netflix or Disney+.

Is piracy still a problem in 2026?

Piracy declined sharply during the 2012-2018 period when Netflix offered broad, affordable access, but has increased again as streaming fragmented and prices rose. Analytics firms tracking piracy traffic reported meaningful increases beginning around 2022-2023, correlated directly with content being pulled from affordable services and placed behind additional paywalls. Netflix’s 2023 password-sharing crackdown also drove some users back to illegal alternatives. The pattern confirms what researchers argued in the early 2010s: piracy rises when legal alternatives are expensive and inconvenient, and falls when they aren’t. It remains a persistent background problem for the industry rather than an existential crisis.

3")

I would like to say that many people are like yourself in noting that a good majority of cinema is “watch-and-forget,” however the movie industry relies on the fact that many people do not see these movies this way. I would argue that many people would watch “The Ugly Truth” or the “Transporter” and find some sort of legitimacy in them, as ridiculous as that sounds.

I guess what I mean is there is a bit of subjectivity that goes into what should be cheaper. But otherwise I agree, but the movie industry thrives on mindless people who consume these movies, and therefore will never agree.

@ Arthur – the Ugly Truth was hilarious and the Transporter was awesome within it’s genre. The fact that you picked these out as crap movies proves your point. You probably liked The Hurt Locker and the Blind Side, movies that I can barely sit through for free. But the writer’s point still stands – I only saw those flicks because I could do so for free. The internet makes it easy to watch stuff you consider crap, and gives you a devalued sense of movies overall.

I like this article. I think we all want the movie industry to be profitable enough to keep making good movies without people having to pay >$20 per movie. NetFlix may be the beginning to the answer.

Another issue that Hollywood faces and could easily is fix piracy is just plain easier. Its easier to get the content. Its easier to get the content to work on multiple devices. The content always just works. The lack of DRM means its less prone to weird errors that can take hours to get fixed if at all and you arent put through 10 extra steps.

They need to make it easy and affordable. If the content was cheaper people would buy more. Volume would make up for the change in overall price.

Model is very good and easy to use.

Despite the poor grammar throughout the article, many good points were made.

Two months ago I dropped DirecTV at $100+ per month, bought a Roku, and went to Netflix at $8 per month. I don’t miss satellite. True, not everything is available, but Netflix can mail out DVDs for a couple bucks extra, and there’s a Redbox a block away, and I can see what’s there and reserve my copy from my iPhone before I even leave home. And I don’t miss the really good shows like The Big Bang Theory because I just pick up the DVD set when the season is over. And for local stuff I got a cheap antenna to pick up local digital broadcasts. I found about 6 good channels in my area.

I have to agree completely with this article. It’s no longer about the value of the content – the real value is in the delivery. Think about it: why are DVRs so popular? They convert broadcast content into on-demand content. The future is here and there’s no going back.

The movie industry is convinced of one simple proposition: people must pay a set price for one piece of content. $30 for a Blu-Ray, $20 for a DVD, $6 for an HD rental and so on.

And in 5 Years Green Ray, and in 15 Years Purple Ray etc…

The movie industry wants you to continually buy the same content over and over…

Screw You George Lucas.

Cut the Cable people. Time Warner, Comcast, Cox are on the ropes for their high prices. I can’t belive the crap I see advertized on T.V. Do we really need to see the home life of Joan Rivers? Cut the crap and stream what YOU want to watch. Movies are the same. Screw the theaters overpriced BS. Stream it! The future is now!

A good question to answer for any home owner who is considering selling their home is, “What’s my

house worth?” Finding the answer to this can be a simple process if just a few easy steps are

followed. There are several options available for homeowners to choose from when determining their

home valuation: appraisals, searching the internet, and consulting a real estate professional are

just a few.

Actually, there is some sort of influence, some sort of manipulation, which seems to come through all movies, and even TV Series, these days. The homosexual bent, and mindless “follow the leader”, and “be one of the social network group”, comes through the content, and messages, with unending, boring, and mind-manipulating glory. In short, the messages in the media suck, the writers appear as if they are teenagers on drugs, and the movies just lack luster.

Frankly, I think it is actually their new anti-pirate tactic(s), and truth is, this tactic(s) are working! And that tactic is, “Simply make movies no one would steal, let alone watch!”

Diabolical really, think about it … 🙂